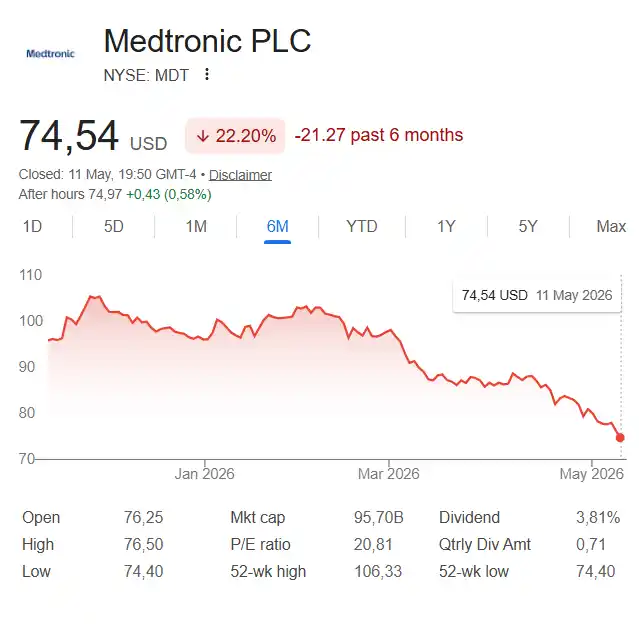

In recent weeks, much of the spine market discussion has focused on Globus Medical and the negative market reaction that followed otherwise strong operating results. But Globus is not alone. Medtronic, one of its most direct competitors in spine technology, has also been under pressure. Its stock recently hit a reported 52-week low at $77.15, and by May 11, 2026, was quoted even lower at $74.54, almost 30% below its 52-week high of $106.33.

That matters because Medtronic has not been standing still. In February, the company received FDA clearance for Stealth AXiS, its next-generation spine platform integrating planning, navigation and robotics into a single system. In April, the platform also received CE Mark in Europe. On paper, this is exactly the type of technology story that should support investor confidence. Yet the stock market reaction tells a more complicated story.

Market and Company Context

Medtronic remains one of the largest and most diversified medtech companies in the world. In its fiscal third quarter 2026, the company reported revenue of $9.017 billion, up 8.7% as reported and 6.0% organically. It also reiterated fiscal 2026 organic revenue growth guidance of approximately 5.5% and non-GAAP EPS guidance of $5.62 to $5.66.

At first glance, these numbers do not look like a company in crisis. Cardiovascular was particularly strong, with reported growth of 13.8% and organic growth of 10.6%. Diabetes also grew 8.3% organically. Neuroscience, which includes Cranial & Spinal Technologies, was more modest: revenue increased 4.1% as reported and 2.5% organically, with Cranial & Spinal Technologies described as growing in the mid-single digits.

This difference is important. Medtronic’s overall innovation narrative is broad, but spine investors are looking specifically at whether the company can regain stronger momentum in a market where Globus Medical, Stryker, NuVasive’s legacy assets, DePuy Synthes and other players continue to compete aggressively. The issue is not whether Medtronic has a spine business. It clearly does. The issue is whether that business can accelerate enough to change the equity story.

Why the Stock Is So Low

The stock weakness appears to reflect a mix of factors rather than one single problem.

First, investors may be questioning the pace of earnings leverage. Medtronic is growing, but the market is not only rewarding revenue expansion. It wants evidence that growth can translate into sustained margin improvement, EPS acceleration and stronger capital efficiency. The company’s own Q3 release referenced tariff impact assumptions of approximately $185 million, which is a reminder that external cost pressures remain part of the model.

Second, Medtronic’s portfolio is complex. It operates across cardiovascular, neuroscience, medical surgical and diabetes. That diversification reduces dependence on any one market, but it can also make the investment thesis harder to read. A strong PFA story, a diabetes separation, a spine robotics launch and margin guidance all sit inside the same equity narrative. For investors, the question becomes: which growth drivers are material enough to re-rate the stock?

Third, the MiniMed separation adds another layer of uncertainty. Reuters reported that Medtronic cut its fiscal 2026 profit forecast to $5.50–$5.54 per share, citing a one-time charge of about $157 million related to a research collaboration and the planned U.S. IPO of MiniMed. That type of adjustment may not directly change the long-term value of the spine business, but it can affect investor perception of near-term earnings quality.

Fourth, the market may be demanding proof that robotics can become a commercial engine, not just a regulatory milestone. Stealth AXiS is strategically significant. Medtronic describes it as a platform that brings planning, navigation and robotics together for spine surgery, with LiveAlign segmental tracking to visualize spinal motion and alignment in real time without repeated imaging.

But FDA clearance and CE Mark are not the same as rapid adoption. Hospitals will still evaluate workflow integration, surgeon preference, capital budgets, installed-base compatibility, service levels and procedural pull-through. In spine robotics, the commercial value is not only the robot. It is the ecosystem around the robot: implants, navigation, imaging, planning software, disposables, training and account control.

What This Means for the Spine Market

For spine implant executives and distributors, Medtronic’s share price weakness should not be read as a sign that robotics is losing relevance. The opposite may be true. The pressure on Medtronic suggests that the market now expects robotics and enabling technology to produce measurable commercial outcomes.

That is also why the comparison with Globus matters. Globus has built much of its strategic narrative around a closed-loop spine ecosystem, combining implants, enabling technologies, robotics, navigation and procedural execution. Medtronic is moving in the same direction with AiBLE and Stealth AXiS. The difference is that Medtronic is much larger and more diversified, which can make spine-specific momentum less visible inside the broader group.

In Medtronic’s Q3 commentary, management described Stealth AXiS as a system designed around navigation, noting that navigation drives a large portion of U.S. spine procedures and that the platform is intended to reduce barriers for surgeons moving into robotics. The company also referenced a large installed base as part of its strategic advantage.

That is a credible argument. But investors will likely want to see whether this installed base translates into conversions, new placements, higher implant pull-through and stronger CST growth. In other words, the next stage is not about whether the technology is interesting. It is about whether it changes the growth profile.

Conclusion

Medtronic’s 52-week low should not be interpreted as a sign of weakness in its underlying assets. The company still has scale, clinical reach, a broad technology base, a large installed footprint and one of the most relevant positions in spine robotics. Few companies can match that combination.

But the market is clearly asking for more than strategic potential. The current share price suggests that investors are not yet convinced that Medtronic can convert those assets into faster growth, better operating leverage and a stronger equity story in the near term.

That makes June 3, 2026 an important date. Medtronic’s fourth-quarter and full-year results should give the market a clearer view of revenue momentum, margin assumptions, the MiniMed separation process and, for the spine sector, any further signals around Cranial & Spinal Technologies and Stealth AXiS.

###

Legal Disclaimer:

Content published on SPINEMarketGroup (thespinemarketgroup.com) is provided for informational purposes only and on an “as is” basis, without warranties of any kind. We do not guarantee the accuracy, completeness, legality, or reliability of any information, images, videos, links, or third-party materials featured on the site. Any views or claims expressed in contributed content or press releases belong to their respective authors or sources. For copyright concerns, factual corrections, or content-related complaints, please contact us directly for review.