Globus Medical is not simply entering 2026 with an “aggressive” posture. It is attempting something structurally more ambitious: building a self-reinforcing spine ecosystem that compresses competitive space around it. This is not a growth story. It is a control story.

Spine as the Economic Engine

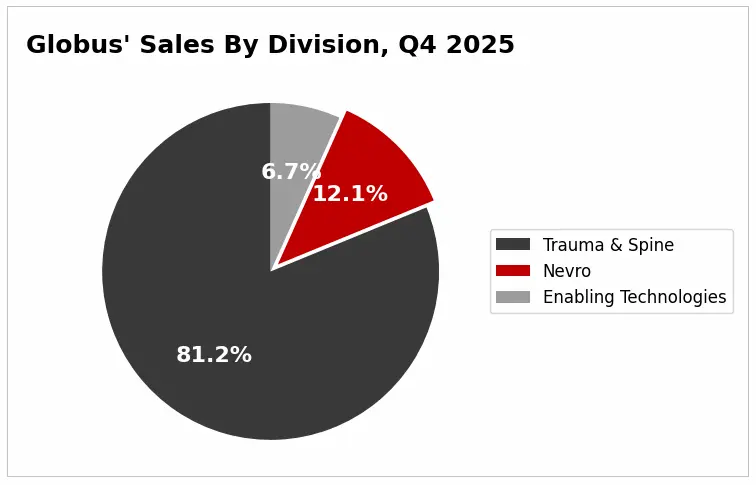

Roughly 95% of revenue still comes from spine. Over 80% of that from the U.S. That level of concentration would normally look like risk. In Globus’ case, it functions as leverage.

U.S. spine returned to sustained growth in the second half of the year, with double-digit expansion in Q3 and Q4. Management highlighted:

- Aggressive commercial recruiting

- Continuous product launches

- Pull-through from robotic placements

- Integration benefits following the NuVasive acquisition

The spine franchise is not just stable. It is the financial backbone funding expansion in adjacent platforms.

And that matters.

Because the smaller segments are not independent growth bets.

They are force multipliers for the implant engine.

Robotics: Placement Over Prestige

Globus’ enabling tech segment, centered around ExcelsiusGPS, faced delays in capital placements earlier in the year. The result was revenue volatility and investor anxiety. But here is the strategic lens:

- Robotics is not being positioned as a standalone profit center.

- It is being positioned as an account control mechanism.

ExcelsiusGPS competes directly with platforms from Medtronic and Stryker. This is not a technology novelty battle. It is a footprint battle.

More placements mean:

- Embedded navigation workflows

- Procedural standardization

- Implant pull-through

- Increased switching friction

Management’s shift toward more flexible deal structures in 2026, including cash placements, signals urgency. Revenue timing matters. But account penetration matters more.

Once a robot is embedded, the relationship changes. And relationships in spine are everything.

Neuromodulation: Extending the Patient Lifecycle

The acquisition of Nevro for $250 million was easy to underestimate. It should not be.Neuromodulation extends Globus’ reach beyond structural repair into chronic pain management.

Strategically, this does three things:

- Broadens surgeon relationships

- Enables cross-selling between spine and pain specialists

- Expands margin potential through operational integration

While standalone Nevro sales declined year-over-year, adjusted EBITDA margins improved meaningfully. The integration phase appears focused on profitability discipline rather than top-line theatrics.

This is not diversification for its own sake.It is vertical depth within the same care continuum.

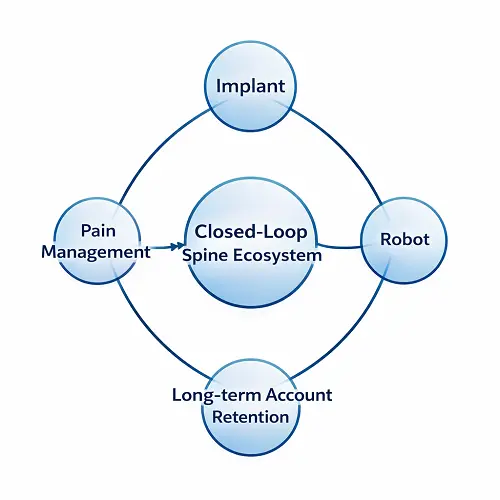

The Structural Question: Is Globus Creating a Closed Loop?

Take a broader view:

- Spine implants generate revenue.

- Robotics reinforces implant usage.

- Neuromodulation extends the therapeutic arc.

- Commercial recruiting reinforces procedural density.

This begins to resemble a closed-loop system:

Robot → Implant → Pain Management → Long-term Account Retention

If robotics becomes a prerequisite in high-value accounts, companies without enabling tech platforms risk structural exclusion. They may survive in price-sensitive segments, but premium procedural environments will consolidate around integrated players.

In that context, Globus is not just competing with large strategics: It is compressing the mid-market from above.

Execution Risk: The Real Variable

The architecture is compelling. The execution burden is heavy.

Globus must simultaneously:

- Sustain U.S. spine momentum

- Accelerate robotic placements without margin erosion

- Integrate Nevro without cultural friction

- Maintain product innovation cadence

That is operational intensity on multiple fronts. If managed well, Globus transitions from a high-performing spine specialist to a structurally integrated spine platform. If mismanaged, concentration risk and capital intensity could amplify volatility.

Why This Matters for the Spine Market?

The broader implication is not stock price appreciation. It is competitive structure. If integrated ecosystems outperform single-product companies, the mid-tier spine landscape could fragment further, forcing:

- Strategic partnerships

- Platform acquisitions

- Niche specialization

- Or private equity roll-ups seeking scale

Globus’ 2026 posture may therefore signal something larger than internal growth ambition. It may signal the next phase of competitive compression in spine.

####